Hundreds of billions are coming to market this year – SpaceX leads the way

According to forecasts, we may see a record-breaking IPO volume of approximately $225 billion in 2026. Combined with capital raises by tech giants already listed on the stock market, this figure could reach as high as $675 billion.

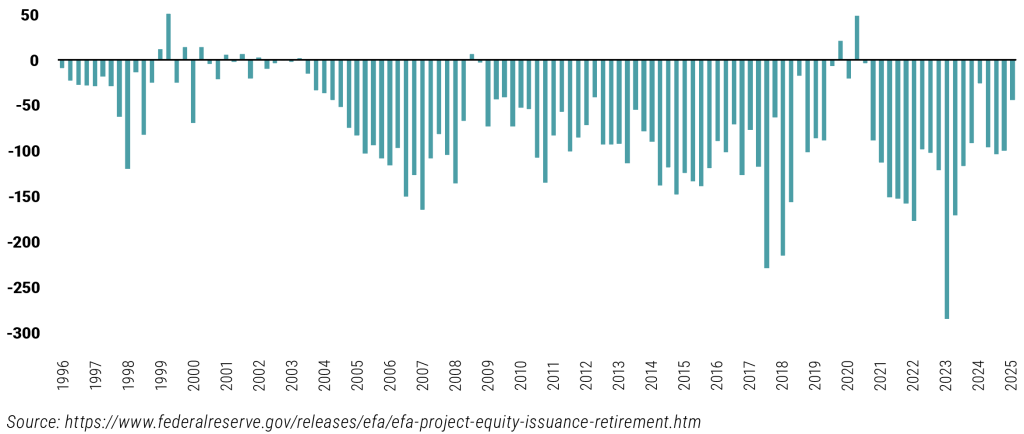

SpaceX’s market debut broke a trend of shrinking IPO activity that had persisted since roughly 2003. Over the past two decades, the development of private capital markets has allowed young companies to remain private for longer, leading to a decline in the number of companies going public. On the other hand, net share issuance by publicly traded companies had been negative for more than twenty years; in other words, companies withdrew more shares from circulation through buyback programs than they issued. Finally, private equity funds also contributed to this trend by acquiring publicly traded companies and taking them back to the private market.

Now, however, a significant shift appears to be underway. Instead of buying back shares, the world’s largest technology companies are investing their money in AI infrastructure and are even preparing for capital raises on an unprecedented scale to finance it. Meanwhile, AI companies valued at trillions of dollars on the private market, including Anthropic and OpenAI, are lining up to go public.

Net Equity Issuance (USD BN)

SpaceX was the first to enter the market

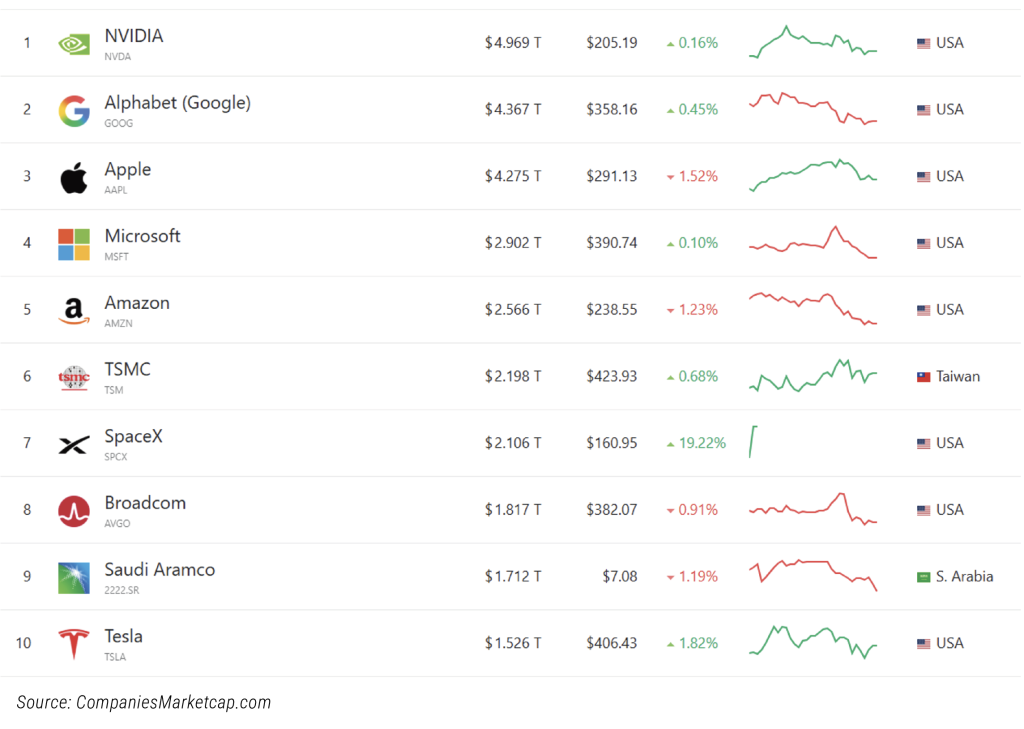

Elon Musk’s space and AI company, SpaceX, was the first to enter the market. As a first step, Musk consolidated X, xAI, Starlink, and SpaceX, all of which were private companies associated with him. The resulting giant, which retained the SpaceX name, debuted on the Nasdaq on June 12 under the ticker symbol SPCX with a valuation of $1.75 trillion.

The record $75 billion raised represents only about a 5% stake in the company. Unusually, the IPO price was not determined by the underwriting investment banks through bookbuilding, but was set at $135 at Musk’s discretion. An unusually large 30% allocation was set aside for retail investors, many of whom are Musk’s most enthusiastic supporters. Retail investor interest resulted in a sevenfold oversubscription for the approximately $25 billion worth of shares available to them.

Goldman Sachs and Morgan Stanley were the lead underwriters, and there was fierce competition for the lead position. Morgan Stanley reportedly took offense at being placed second behind Goldman Sachs in the top-left “lead-left” position of the S-1 filing due to alphabetical order.

The first day of trading proved to be a success. Secondary market trading opened at $150 and reached as high as $176 during the day, raising SpaceX’s valuation to roughly $2.2 trillion. This market capitalization ranks it seventh on the list of the world’s largest companies.

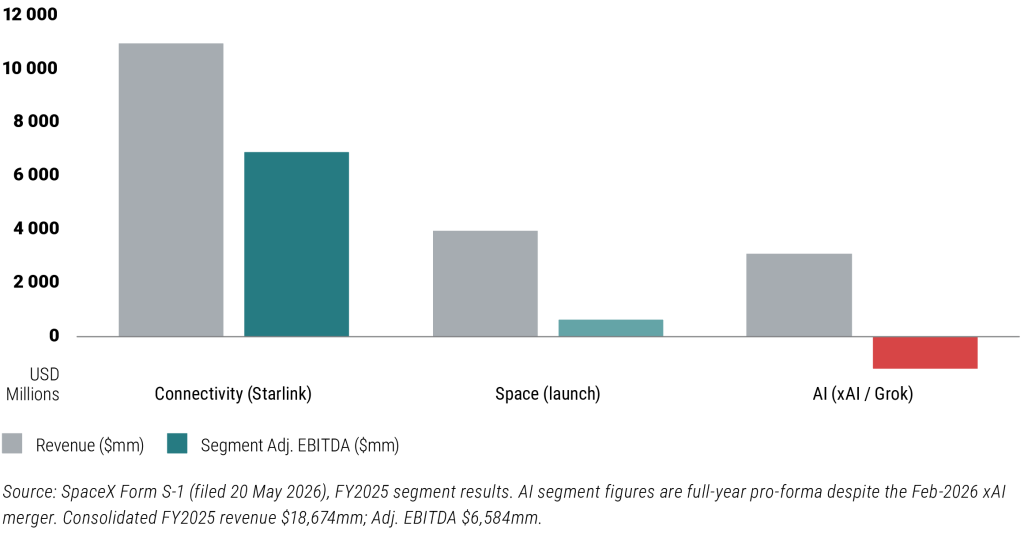

However, it is questionable whether its position on the list of the largest companies is supported by its fundamentals. Alongside its sky-high valuation of $1.75 trillion, the company’s revenue for 2025 is a mere $18.7 billion. This means the stock is trading at a price-to-revenue ratio of 94, which is an unrealistically high figure even by traditional price-to-earnings ratio standards. The company is expected to remain unprofitable in 2026, and even the most optimistic estimates place profitability several years down the road.

FY2025 Segment Revenue vs. Segment Adjusted EBITDA

Return Download

This is a marketing communication. Making a well-informed investment decision requires obtaining detailed information. Please read the Key Information Document, the official prospectus, and the management regulations available at the distribution points of the Fund and on the website of the Fund Manager (www.vigam.hu) for detailed information regarding the Fund’s investment policy, distribution costs, and the possible risks of investing. Costs related to the distribution of the investment fund (purchase, holding, sale) can be found in the Fund’s management regulations and at the distribution points. Past performance is not a reliable indicator of future returns. Future returns from the investment may be subject to taxation, and tax and duty information relating to individual financial instruments and transactions can only be accurately assessed based on the individual circumstances of each investor, which may change in the future. It is the investor’s responsibility to obtain information regarding tax obligations.

The data contained in this information material are provided for informational purposes only and do not constitute investment advice, an offer, or investment consulting. VIG Investment Fund Management Hungary Ltd. accepts no liability for investment decisions made based on this information or for their consequences. The license number of the Fund Manager for alternative investment fund management (AIFM) is: H-EN-III-6/2015. The license number of the Fund Manager for UCITS fund management (collective portfolio management) is: H-EN-III-101/2016.