AI’s financial web

How Nvidia and OpenAI fuel the AI money machine

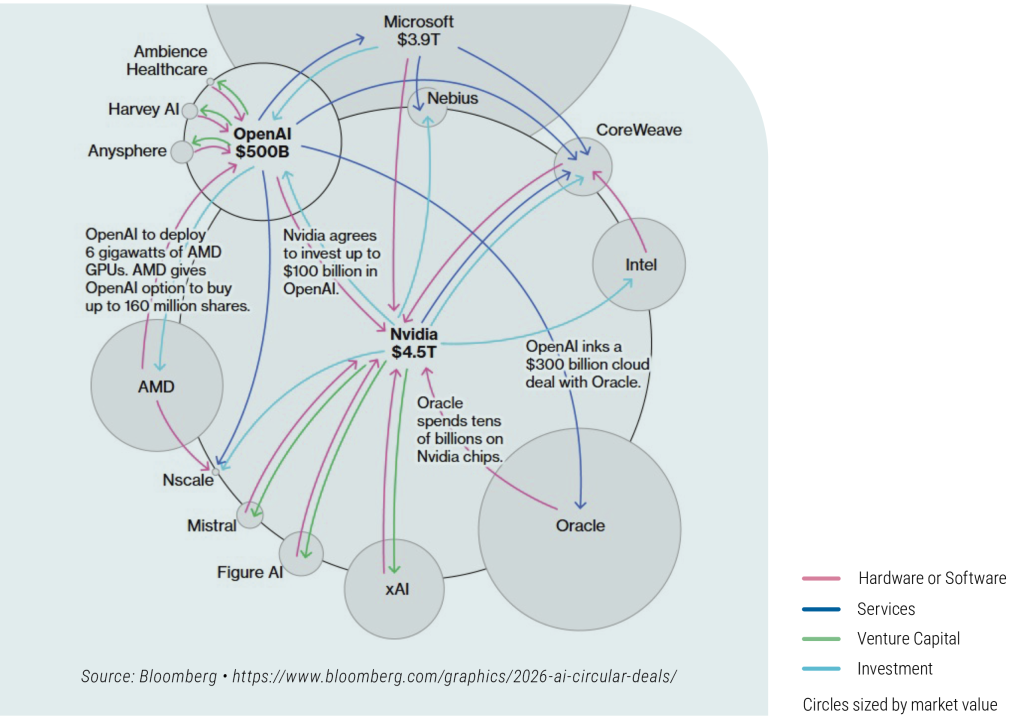

One of the most talked-about visuals of 2025 regarding AI trends was a chart published by Bloomberg that illustrated the circular nature of financing in the tech sector. It sought to highlight that, in the sector, the same dollars are often recycled over and over again, potentially inflating the true picture of demand for chips, AI, and computing capacity. This type of financial innovation has since become much more widespread in the ecosystem, and there is hardly an AI player that isn’t part of multiple transactions that create mutual dependencies.

For example:

- Nvidia is known for its venture-capital-style investments, often within its own industry or even at a lower level in the supply chain. This in itself is a perfectly acceptable and rational activity. The problem arises because cloud service providers like CoreWeave serve as both an investor and a customer for Nvidia. The chip giant first purchases a stake in the company worth several billion dollars, and then, due to the cloud service provider’s business model, spends nearly 100% of the invested amount on Nvidia chips to build out its hardware infrastructure. In this way, Nvidia effectively finances its own demand; in fact, it often enters into so-called “backstop” agreements with such companies, committing to repurchase the cloud service provider’s unused computing capacity, including chips that are idle. This reduces the cloud company’s credit risk in the eyes of investors, as one of the world’s most profitable companies provides a guarantee for the loan portfolio, which is backed by Nvidia chips and appears on the cloud company’s balance sheet. Under this structure, Nvidia effectively emerges with artificially inflated revenue and a growing stock portfolio, while the neocloud company benefits from a better-than-deserved credit rating and a secure source of capital.

- Another common structure involves exchanging computing capacity for equity. The most typical example of this is the complex relationship between Microsoft and OpenAI. A significant portion of the nominal amounts invested in AI labs often comes not in dollars but in cloud computing capacity credits, for example, from Microsoft to OpenAI. This means that OpenAI can use the Azure cloud platform to the tune of X billion dollars, in exchange for which it receives hyper-scalable OpenAI stock. Microsoft later reports this cloud demand as growth and revenue in its cloud division, which has become the main growth engine for giant tech companies. In its quarterly reports, Microsoft not only reports cloud revenue, which is essentially financed with its own money, but also reflects the impact of OpenAI shares in the appreciation of investments, which has accounted for an increasingly large portion of its profits in recent quarters.

- But this is still far from the strangest deals out there. AMD’s demand-for-shares swap structure is already in the running for that title. The company swapped two 10% stakes in the form of warrants with OpenAI and Meta in exchange for the latter two using AMD chips to build out their AI computing capacity at a scale of several gigawatts. In doing so, the chip manufacturer is paying, by diluting existing shareholders, to create its own demand. The agreement grants customers nearly $100 billion worth of equity stakes and dramatically increases AMD’s order backlog.

All of these can be problematic because they create opaque interdependencies within the ecosystem. These circular transactions help postpone economic reality in the short term and send both the market and apparent fundamentals soaring. However, should the trend begin to slow or unexpectedly break, the network of tightly intertwined companies could trigger a violent, reflexive swing in the opposite direction.

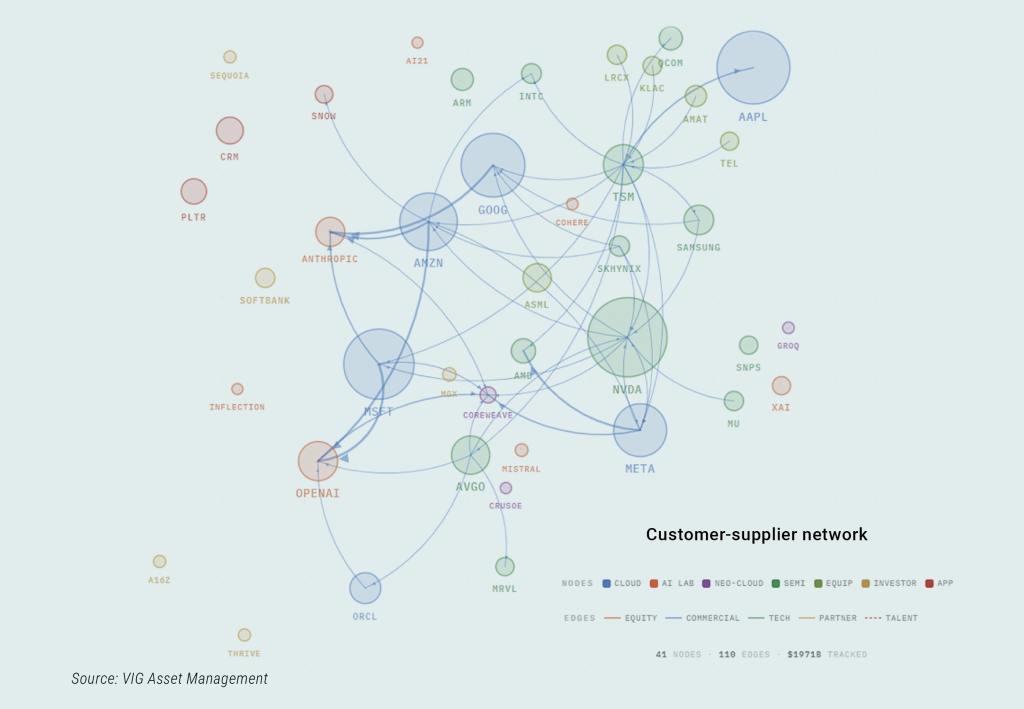

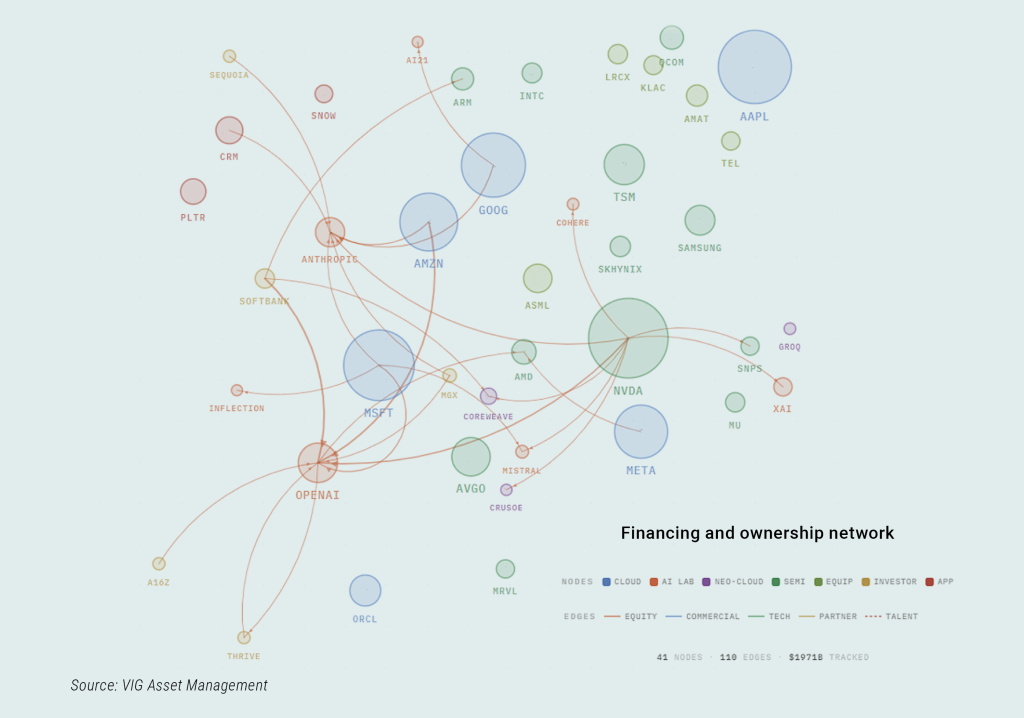

This list is by no means exhaustive, but the network diagram summarizing our research aims to illustrate the extent of interconnectivity among tech companies that invest in one another and, in some cases, finance their own demand.

Customer-supplier network

Financing and ownership network

Return

Download

Return

Download

This is a marketing communication. Making a well-informed investment decision requires obtaining detailed information. Please read the Key Information Document, the official prospectus, and the management regulations available at the distribution points of the Fund and on the website of the Fund Manager (www.vigam.hu) for detailed information regarding the Fund’s investment policy, distribution costs, and the possible risks of investing. Costs related to the distribution of the investment fund (purchase, holding, sale) can be found in the Fund’s management regulations and at the distribution points. Past performance is not a reliable indicator of future returns. Future returns from the investment may be subject to taxation, and tax and duty information relating to individual financial instruments and transactions can only be accurately assessed based on the individual circumstances of each investor, which may change in the future. It is the investor’s responsibility to obtain information regarding tax obligations.

The data contained in this information material are provided for informational purposes only and do not constitute investment advice, an offer, or investment consulting. VIG Investment Fund Management Hungary Ltd. accepts no liability for investment decisions made based on this information or for their consequences. The license number of the Fund Manager for alternative investment fund management (AIFM) is: H-EN-III-6/2015. The license number of the Fund Manager for UCITS fund management (collective portfolio management) is: H-EN-III-101/2016.