First signal or one-off outlier? Why cybersecurity stocks surged after late April?

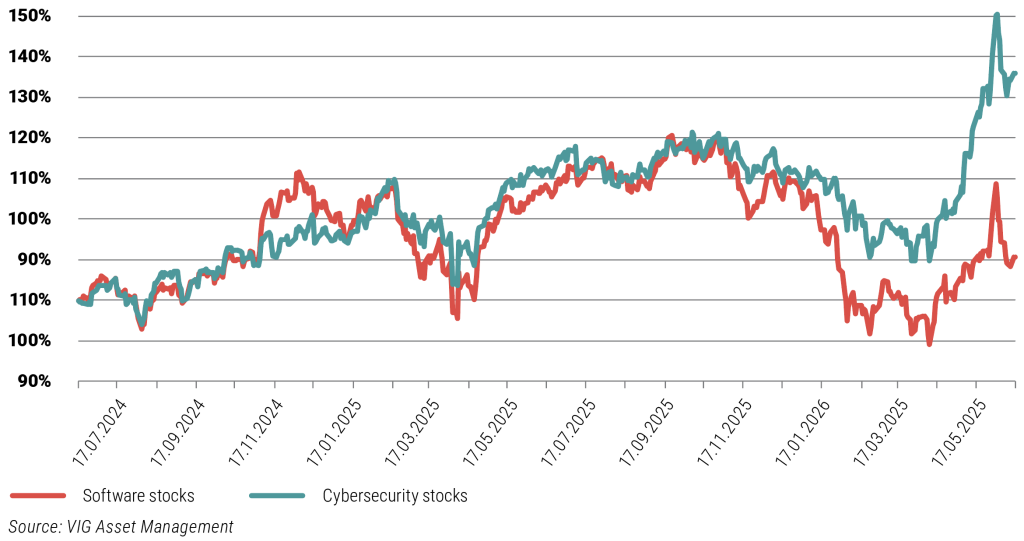

While the broader software market (SaaS) continues to underperform the broader markets, with the exception of a short-covering rally (which we covered in detail in last month’s Megatrend Monitor), the cybersecurity sector has staged a spectacular rally since the end of April. The leading companies in the cybersecurity sector (Palo Alto Networks, CrowdStrike, Cisco, Fortinet) have posted massive gains of over 70% since the end of April.

But what is behind this sudden surge, and is cybersecurity the “first sign” of a broader recovery in the software sector that will pull other software stocks along with it?

1. From collective panic to a reality check

To understand the spring surge in cybersecurity stocks, it’s worth looking back to the beginning of the year. In the first months of 2026, a significant sell-off swept through the entire cloud-based and subscription-based software market, resulting in a sharp decline of about 20% by March.

This nosedive was primarily fueled by fears that next-generation artificial intelligence (such as Anthropic’s latest models) would fundamentally disrupt the market. Investors feared that super-intelligent systems would render traditional software obsolete, or that companies would prefer to spend money on their own AI developments at the expense of cybersecurity. At this stage, the stock market was not yet discriminating: cybersecurity stocks were punished just as severely as companies producing HR or marketing software.

By the end of April, however, a radical turnaround occurred. The market realized that generative AI is not only failing to destroy cybersecurity companies but is, in fact, a powerful engine driving their growth.

The sector’s sudden surge was caused by a fortunate convergence of the following factors:

- The AI arms race: Companies realized that hackers are also using AI to carry out more complex attacks. As a result, state-of-the-art defense platforms, which are also built on artificial intelligence (such as XDR and SASE systems), suddenly became indispensable.

- Revenue stability: Spring quarterly financial reports showed that cybersecurity companies’ order books and future growth prospects remained rock-solid, and management teams issued extremely optimistic forecasts.

- Government and legal pressures: State-sponsored cyberattacks have proliferated due to global geopolitical conflicts. At the same time, tightening international and U.S. regulatory requirements (such as the mandatory, rapid reporting of cyber incidents) have made strengthening their cybersecurity a legal obligation for companies.

The improved perception of cybersecurity companies has triggered a spectacular inflow of capital. It is important to note, however, that this spring rally has so far been driven primarily by improving market sentiment and a shift in positioning, after the sector became unreasonably undervalued during the panic at the beginning of spring.

The biggest question for the coming quarters is now to what extent this surge in confidence and higher valuation levels will be reflected in concrete, tangible financial fundamentals (accelerating revenue growth, improving free cash flow). If the volume of corporate orders justifies the current optimism, the rally could prove to be sustainable.

2. Sentiment vs. fundamentals: can the rally last?

The improved perception of cybersecurity companies has triggered a spectacular inflow of capital. It is important to note, however, that this spring rally has so far been driven primarily by improving market sentiment and a shift in positioning, after the sector became unreasonably undervalued during the panic at the beginning of spring.

The biggest question for the coming quarters is now to what extent this surge in confidence and higher valuation levels will be reflected in concrete, tangible financial fundamentals (accelerating revenue growth, improving free cash flow). If the volume of corporate orders justifies the current optimism, the rally could prove to be sustainable.

3. First signal, or just a defensive outlier?

Is the success of cybersecurity a harbinger of a resurgence in the software sector in the broader sense, or is this field following a completely different path?

There is a fundamental structural difference between traditional software vendors (HR systems, customer relationship management software, office applications) and cybersecurity, the difference is about priority.

A company can postpone updating its marketing software or purchasing new licenses if it wants to cut costs. But it cannot disable its firewall or data protection, because a single successful ransomware attack could lead to the company’s immediate bankruptcy. For this reason, cybersecurity is much more resilient to macroeconomic cycles and temporary freezes on corporate budgets compared to more traditional software vendors. It is one of the few areas of the software industry where the growth rate can accelerate even in a more challenging economic environment.

Although cybersecurity has its own specific drivers, its success nevertheless sends a positive signal to the entire tech market:

After stock market growth over the past year and a half was driven almost exclusively by hardware manufacturers (Nvidia, Broadcom) and cloud service giants, cybersecurity has shown investors that there is also enormous potential in pure-play software models. This could restore the market’s overall confidence in software stocks. Cybersecurity companies are the first to have successfully integrated AI features, such as AI-powered assistants, and are selling them at a premium, generating real profits. As soon as the market sees that other major software companies are also capable of generating tangible additional revenue from intelligent features, capital may start flowing their way as well.

Summary

Since the end of April, the cybersecurity sector has demonstrated that the market is capable of quickly correcting excessive AI fears. The sector has decoupled itself from the broader software market’s slump, and investors have recognized the growth potential inherent in artificial intelligence.

Although it cannot be considered a classic “first sign” that automatically pulls all other software companies along with it, cybersecurity is an excellent example of how both customers and investors are willing to pay for essential technology services even in a more challenging market environment. The broader software market’s recovery will likely be slower and more selective, and will likely be closely tied to who is able to turn AI into real profits.

Return DownloadThis is a marketing communication. Making a well-informed investment decision requires obtaining detailed information. Please read the Key Information Document, the official prospectus, and the management regulations available at the distribution points of the Fund and on the website of the Fund Manager (www.vigam.hu) for detailed information regarding the Fund’s investment policy, distribution costs, and the possible risks of investing. Costs related to the distribution of the investment fund (purchase, holding, sale) can be found in the Fund’s management regulations and at the distribution points. Past performance is not a reliable indicator of future returns. Future returns from the investment may be subject to taxation, and tax and duty information relating to individual financial instruments and transactions can only be accurately assessed based on the individual circumstances of each investor, which may change in the future. It is the investor’s responsibility to obtain information regarding tax obligations.

The data contained in this information material are provided for informational purposes only and do not constitute investment advice, an offer, or investment consulting. VIG Investment Fund Management Hungary Ltd. accepts no liability for investment decisions made based on this information or for their consequences. The license number of the Fund Manager for alternative investment fund management (AIFM) is: H-EN-III-6/2015. The license number of the Fund Manager for UCITS fund management (collective portfolio management) is: H-EN-III-101/2016.