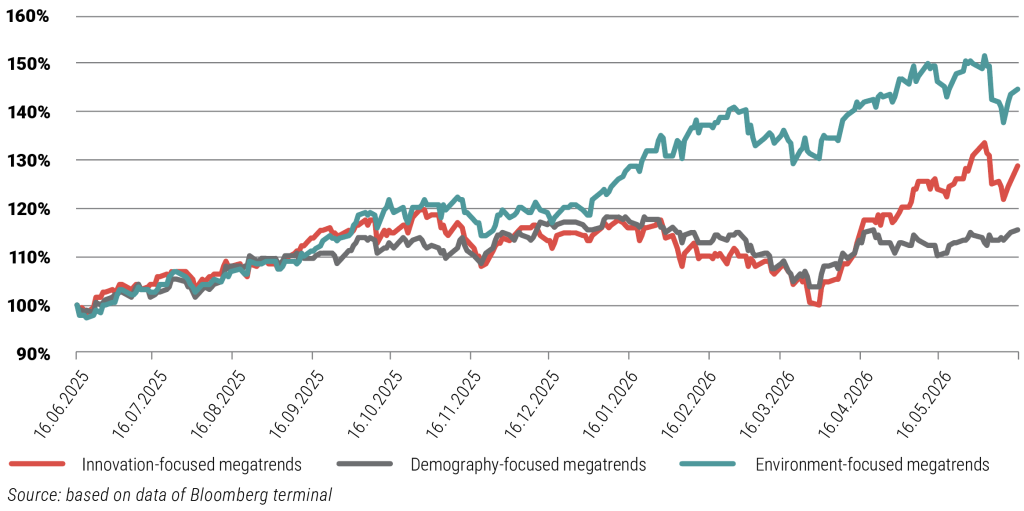

Performance of Megatrends

When examining the performance of the three main strategies (innovation-, demography-, and environment-focused megatrends) within the megatrend universe, we have witnessed an extremely exciting and dynamic realignment in recent times. Although, over the longer, one-year time horizon, environment-focused megatrends still confidently lead the pack with an annual return of approximately +45%, ahead of innovation-focused strategies at +29% and demographic strategies at +16%, over the past month, there has been a radical shift in market narrative and capital flows.

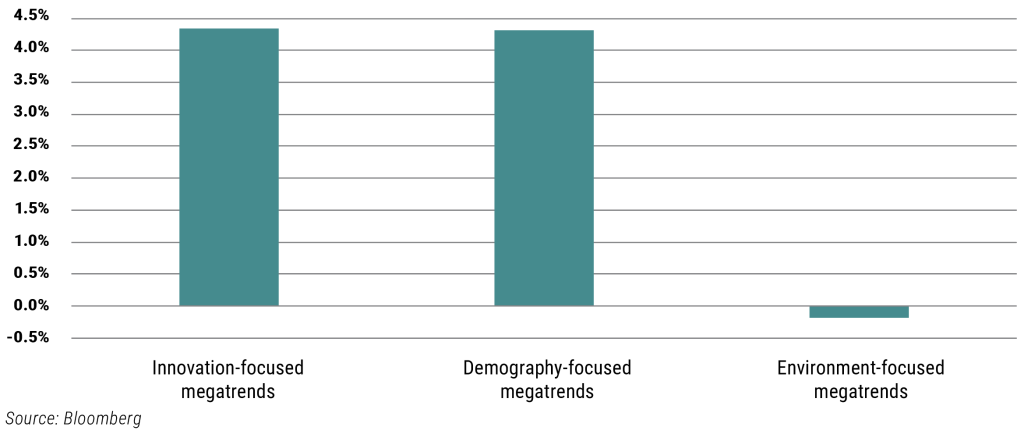

While earlier this spring we were discussing how the geopolitical uncertainty caused by the conflict in Iran and the unprecedented energy demands of artificial intelligence had elevated environmental megatrends and sustainable infrastructure to become the true, fundamental drivers of the innovation boom, the past thirty days have seen a sharp wave of profit-taking in green sectors. This slowdown pushed the environment-focused category into a slight decline of -0.2% over the past month. At the same time, growth and technology stories have regained momentum: both innovation-focused and demography-focused megatrends posted a spectacular 4.3% gain in just a single month.

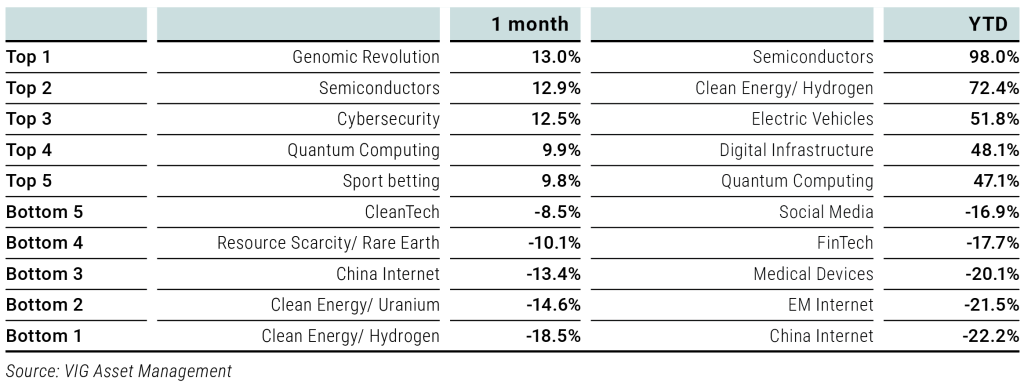

If we look beneath the surface, the monthly performance of the sub-megatrends perfectly illustrates this rotation. The clear winners over the past month were technological and healthcare breakthroughs. The Genomic Revolution rose by 13.0%, Semiconductors by 12.9%, and Cybersecurity by 12.5%, while Quantum Computing and Sports Betting also approached 10% monthly returns. In sharp contrast, the favorites of the previous period, themes related to clean energy, underwent a significant correction: hydrogen (Clean Energy / Hydrogen) fell by 18.5%, uranium (Clean Energy / Uranium) by 14.6%, and clean technologies in the broader sense (CleanTech) by 8.5% over the course of thirty days.

However, looking at year-to-date (YTD) performance, it becomes clear that this monthly dip in the green sectors is, for now, merely a healthy correction within the long-term upward trend. Despite this monthly setback, the clean energy and hydrogen sectors are still up an astonishing 72.4% since the start of the year. In this longer-term race, semiconductors are the clear frontrunners with their 98.0% year-to-date surge, but electric vehicles (+51.8%) and digital infrastructure (+48.1%) are also massive pillars of this year’s growth. At the other end of the spectrum are Chinese internet companies (China Internet), which are grappling with structural problems; with a monthly decline of 13.4%, they are now down 22.2% since the start of the year, but emerging market internet companies (-21.5%) and the fintech sector (-17.7%) are also showing persistent underperformance.

Best and worst performing subsectors:

Overall, the market for megatrends has entered a mature phase, where a temporary lull in environment-focused strategies has provided an opportunity for innovation and demographic themes, whether they had fallen behind or were just gaining new momentum, to catch up. Global structural trends, however, remain unchanged: the hardware requirements of artificial intelligence (semiconductors) and the transition to sustainable energy reinforce one another and, hand in hand, determine the direction of the markets.

Return DownloadThis is a marketing communication. Making a well-informed investment decision requires obtaining detailed information. Please read the Key Information Document, the official prospectus, and the management regulations available at the distribution points of the Fund and on the website of the Fund Manager (www.vigam.hu) for detailed information regarding the Fund’s investment policy, distribution costs, and the possible risks of investing. Costs related to the distribution of the investment fund (purchase, holding, sale) can be found in the Fund’s management regulations and at the distribution points. Past performance is not a reliable indicator of future returns. Future returns from the investment may be subject to taxation, and tax and duty information relating to individual financial instruments and transactions can only be accurately assessed based on the individual circumstances of each investor, which may change in the future. It is the investor’s responsibility to obtain information regarding tax obligations.

The data contained in this information material are provided for informational purposes only and do not constitute investment advice, an offer, or investment consulting. VIG Investment Fund Management Hungary Ltd. accepts no liability for investment decisions made based on this information or for their consequences. The license number of the Fund Manager for alternative investment fund management (AIFM) is: H-EN-III-6/2015. The license number of the Fund Manager for UCITS fund management (collective portfolio management) is: H-EN-III-101/2016.