On your mark, get set, weapon?

Increased military spending in the European Union due to the Russo-Ukrainian war starting in 2022 would change the position of Article 8 (light green) and Article 9 (dark green) funds. The growing geopolitical tensions have prompted the European Commission to launch the ReArm Europe/Readiness 2030 initiative, which aims to strengthen the EU’s military and defense capabilities. By 2030, €800 billion of funding is expected to flow into the sector to accelerate adaptation to the current situation, which may raise concerns about the compatibility of ESG (E – environmental, S – social, G – governance) policies.

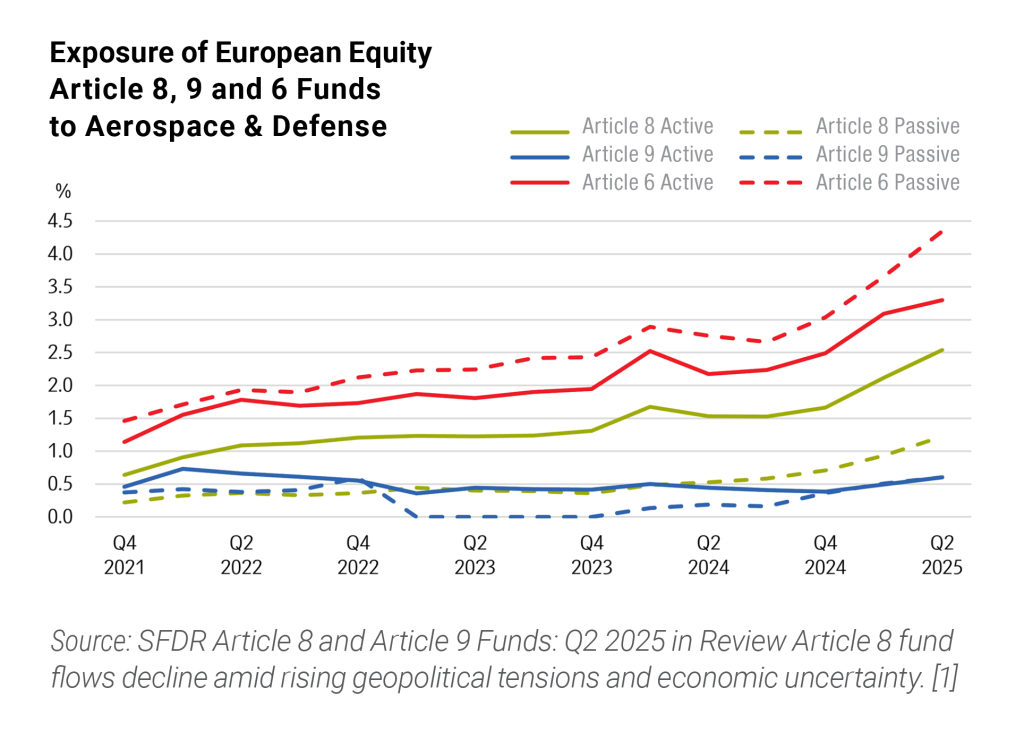

Since the start of the war, inv estors’ general interest in the aerospace and defense industry has been growing, as reflected in the increased exposure to stocks in this sector in Article 6 and 8 funds. However, this trend is not observed in dark green funds.

Over the past three and a half years, both actively and passively managed Article 6 and 8 equity funds have seen a sharp increase in their exposure to the aerospace and defense industry.

Compared to Article 6 funds, Article 8 funds’ exposure to the aerospace and defense industry remains relatively low due to strict exclusion criteria, while Article 9 funds have almost zero exposure to companies active in this industry.

Two main factors may explain the increase in exposure: on the one hand, the increased long positions by fund managers, and on the other hand, the appreciation of defense stocks.

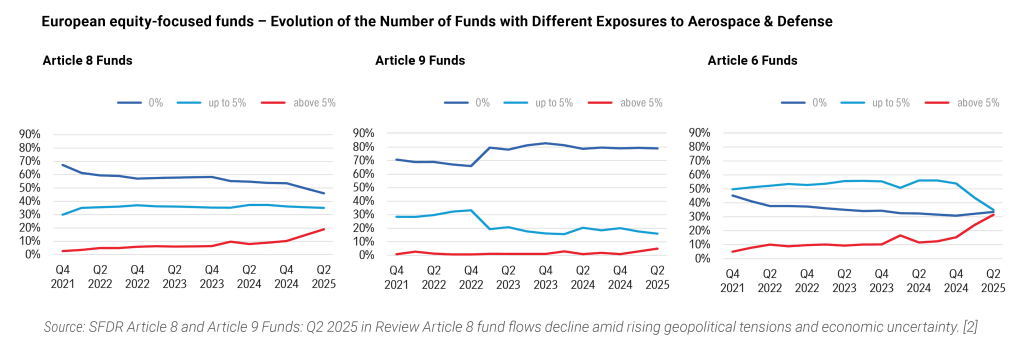

The graphs above show how the exposure of European equity funds has changed over time according to their SFDR classification.

Since 2022, the share of Article 6 and Article 8 funds that state in their prospectus that they exclude controversial weapons from their investments has increased from 19% to 29% at Article 6 funds and from 76% to 92% at Article 8 funds.

As there is no single regulatory definition of the term “controversial weapons”, the types of companies subject to exclusion may vary: some funds exclude only companies that produce controversial weapons, while others also exclude companies that provide components, logistics or support services. In addition, some funds exclude all nuclear weapons-related activities, while others make exceptions for companies based in countries that have signed the Treaty on the Non-Proliferation of Nuclear Weapons (NPT).

This does not mean that the regulatory framework is changing, but there are factors that definitely demonstrate the changing environment of Article 8 and Article 9 funds and are worth monitoring in the future.

We are also closely following the changing environment at VIG Asset Management Hungary, so we reserve the right to change the aerospace and defense exposure of our investment funds in any direction, taking into account the effective external and internal regulations, in order to ensure that our clients benefit from market developments to the greatest extent possible.

The article was based on the analysis of ’SFDR Article 8 and Article 9 Funds: Q2 2025 in Review Article 8 fund flows decline amid rising geopolitical tensions and economic uncertainty’.

[1]-[2]: Bioy, Hortense, et al. SFDR Article 8 and Article 9 Funds: Q2 2025 in Review Article 8 Fund Flows Decline amid Rising Geopolitical Tensions and Economic Uncertainty. Morningstar Sustainalytics , 29 July 2025. Available at: https://assets.contentstack.io/v3/assets/blt9415ea4cc4157833/bltdb931b89f7bc073c/SFDR_Article_8_and_Article_9_Funds_Q2_2025.pdf?utm_source=eloqua&utm_medium=email&utm_campaign=&utm_content=_32731&utm_id= [Accessed 3rd September, 2025]

Jogi nyilatkozat: A blog üzemeltetője a VIG Befektetési Alapkezelő Magyarország Zrt., a szerzői az Alapkezelő munkavállalói. A weboldal kereskedelmi kommunikációt tartalmaz. A blogon megjelenő cikkek magánszemélyek szubjektív véleményét tükrözik, tájékoztatási céllal készülnek és nem minősülnek befektetési elemzésnek vagy befektetési tanácsadásnak és nem tartalmaznak befektetési ajánlást. A blog szerzői saját nevükben kereskedhetnek olyan pénzügyi és pénzeszközzel vagy más termékkel, amelyről az általuk készített cikk közöl tájékoztatást vagy véleményt. Bár a szerzők tőzsdei vagy tőzsdén kívüli kereskedés során szerzett tapasztalata a jelen blogon szereplő írásaikban is megjelenhet, de érdekeltség nem befolyásolhatja az általuk közölt tájékoztatást. A blogon megjelenő cikkekben, hírekben és tájékoztatásokban megjelenhetnek olyan társaságok, amelyek üzleti kapcsolatot tartanak fenn a VIG Befektetési Alapkezelő Magyarország Zrt.-vel vagy a blog szerzőivel akár közvetlenül, akár a VIG Group cégcsoportba tartozó más vállalkozáson keresztül. Jelen blogon megjelent cikkek nem tartalmaznak teljes körű tájékoztatást, és nem helyettesítik a befektetés megfelelőségének vizsgálatát, amelyet csak az adott befektető egyedi körülményeinek értékelésével lehet megállapítani. A megalapozott befektetési döntés meghozatalához kérjük, hogy részletesen és több forrásból tájékozódjon!

A VIG Befektetési Alapkezelő Magyarország Zrt., a blog szerkesztői és szerzői nem vállalnak felelősséget a blogon szereplő tartalom naprakészségéért, esetleges hiányosságaiért vagy pontatlanságaiért, valamint a blogcikkek alapján hozott befektetési döntésekért és a befektetési döntésekből származó bármilyen közvetlen vagy közvetett kárért vagy költségért.