Is Value really dead?

Over the past decade, it has become fashionable to declare value investing dead.

The growth factor has won: large technology stocks and compelling growth stories have dramatically outperformed traditional value portfolios. Well-known value benchmarks – such as the S&P 500 Value or the Russell 2000 Value – have underperformed the broad S&P 500 for most of the period. This is where the narrative comes from: book value, the balance sheet, and the income statement are outdated, and value investing belongs to the past.

The strategy presented in this article starts from a different premise: quality value can still work – if we select carefully. Cheap sectors (such as financials or energy) can remain cheap for extended periods, and book-value-based indices often include low-quality companies that are structurally challenged. It is no coincidence that traditional value indices frequently represent a basket that is cheaper, but also of lower quality, than the S&P 500.

Quality value: not just cheap, but high quality

The approach outlined below is based on the idea that quality value can still deliver results – if stock selection is disciplined. We look for companies that are fundamentally strong, financially stable, and not overly expensive.

The portfolio selects from a broad universe of liquid U.S. equities – effectively similar to the Russell 3000 – refined through fundamental and valuation screens. Stock selection rests on three pillars:

1. Improving fundamentals

Using accounting-based metrics, the strategy distinguishes between companies with sustainably positive earnings and improving financial conditions, and those where reported profits are more the result of accounting optics than genuine performance. Key elements of fundamental momentum include positive net income, strong operating cash flow, improving profitability, better liquidity, and a balance sheet that is not artificially inflated.

2. Low bankruptcy risk

The second filter evaluates capital structure, leverage, and asset profitability. This is where the Altman Z-score comes into play – a fundamental bankruptcy probability indicator used for more than 50 years. A higher Z-score signals lower bankruptcy risk. By applying this measure, the strategy seeks to avoid companies with elevated default risk.

3. Relative cheapness

A core element of value investing is low valuation. The greatest price appreciation potential is often found among relatively undervalued stocks. Accordingly, the strategy excludes companies with high P/E and P/B ratios from the investment universe.

The result is a factor-oriented, more concentrated U.S. equity portfolio that deliberately deviates from the market index: more quality value exposure, fewer structurally weak companies. Stocks are equally weighted, and total exposure remains slightly below 100% to avoid unnecessary forced selling due to technical or margin constraints. The strategy is not the result of ex post “cherry-picking,” but of a rules-based, mechanical screening process.

Like any equity portfolio, the strategy is exposed to market drawdowns – particularly when the value style is out of favour. In return, however, each position is backed by explicitly defined, quantifiable fundamental logic.

Results: Quality value vs. SPY (2020–2025)

Period: January 1, 2020 – December 31, 2025

Initial capital: USD 100,000 in each portfolio

Data source: Author’s own calculations

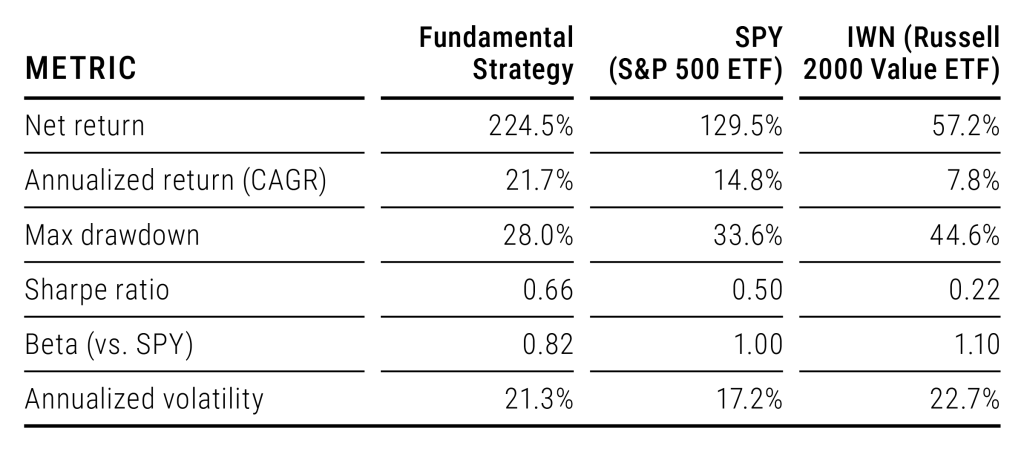

During the period analysed, the fundamental strategy grew to approximately USD 324,500, while SPY reached around USD 229,500, and the IWN ETF (tracking the Russell 2000 Value Index) rose to roughly USD 157,200. The annual return difference versus SPY was about 7 percentage points (21.7% vs. 14.8% CAGR), which is also striking in absolute terms: starting from the same initial capital, roughly USD 100,000 in additional wealth accumulated over six years.

The excess return was not the result of extreme risk-taking. The strategy’s maximum drawdown was smaller than that of SPY (−28% vs. −33.6%), recovery from troughs was faster, and the Sharpe ratio was higher. The information ratio relative to the S&P 500 was positive, suggesting that the active positions taken versus the index reflected consistent, fundamentally grounded excess performance rather than noise. While volatility was higher than that of the benchmarks, this is expected given the strategy’s relatively concentrated structure of 20–30 holdings for most of the period.

Limitations

All of this is based on a back test, not a live track record. The sample period is limited and may have been partially favourable to the value style. Transaction costs, taxation, and data quality may distort the results. It is unrealistic to expect this approach to outperform the market in every environment – particularly during another extreme growth rally.

The key point, however, is not whether this specific rule set will reliably beat the market tomorrow. Rather, it is that a fundamentally driven, quality value strategy is not the same as a simple value benchmark. While the latter often underperform the S&P 500, a thoughtfully constructed and rigorously screened value strategy may still be capable of generating alpha.

The “value is dead” narrative largely reflects the underperformance of superficially constructed value indices. Fundamentally grounded, quality value portfolios, however, can still demonstrate that the information embedded in financial statements has return potential.

Jogi nyilatkozat: A blog üzemeltetője a VIG Befektetési Alapkezelő Magyarország Zrt., a szerzői az Alapkezelő munkavállalói. A weboldal kereskedelmi kommunikációt tartalmaz. A blogon megjelenő cikkek magánszemélyek szubjektív véleményét tükrözik, tájékoztatási céllal készülnek és nem minősülnek befektetési elemzésnek vagy befektetési tanácsadásnak és nem tartalmaznak befektetési ajánlást. A blog szerzői saját nevükben kereskedhetnek olyan pénzügyi és pénzeszközzel vagy más termékkel, amelyről az általuk készített cikk közöl tájékoztatást vagy véleményt. Bár a szerzők tőzsdei vagy tőzsdén kívüli kereskedés során szerzett tapasztalata a jelen blogon szereplő írásaikban is megjelenhet, de érdekeltség nem befolyásolhatja az általuk közölt tájékoztatást. A blogon megjelenő cikkekben, hírekben és tájékoztatásokban megjelenhetnek olyan társaságok, amelyek üzleti kapcsolatot tartanak fenn a VIG Befektetési Alapkezelő Magyarország Zrt.-vel vagy a blog szerzőivel akár közvetlenül, akár a VIG Group cégcsoportba tartozó más vállalkozáson keresztül. Jelen blogon megjelent cikkek nem tartalmaznak teljes körű tájékoztatást, és nem helyettesítik a befektetés megfelelőségének vizsgálatát, amelyet csak az adott befektető egyedi körülményeinek értékelésével lehet megállapítani. A megalapozott befektetési döntés meghozatalához kérjük, hogy részletesen és több forrásból tájékozódjon!

A VIG Befektetési Alapkezelő Magyarország Zrt., a blog szerkesztői és szerzői nem vállalnak felelősséget a blogon szereplő tartalom naprakészségéért, esetleges hiányosságaiért vagy pontatlanságaiért, valamint a blogcikkek alapján hozott befektetési döntésekért és a befektetési döntésekből származó bármilyen közvetlen vagy közvetett kárért vagy költségért.