Gold paradox: why is gold falling when everything would justify a rise?

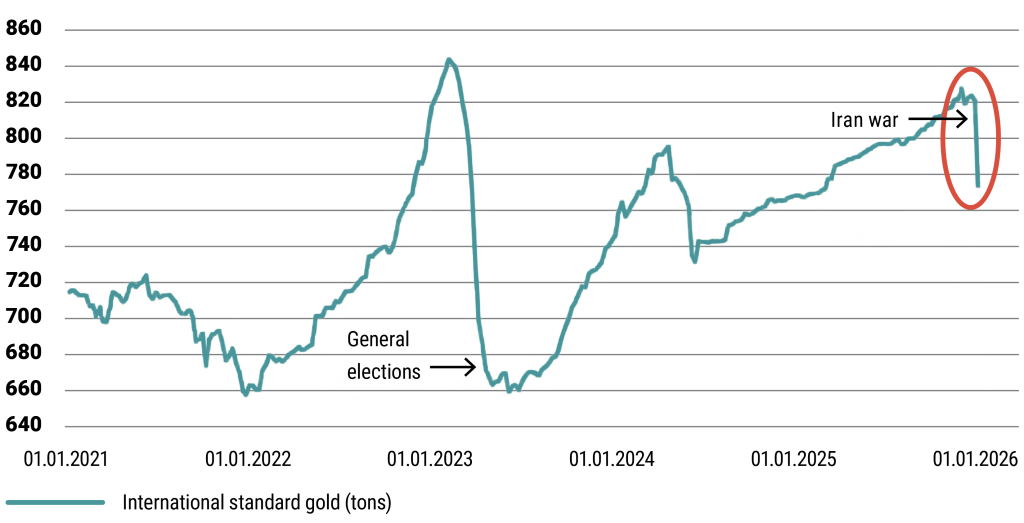

Since the outbreak of the Iran war, the price of gold has declined by around 12% and currently stands at approximately $4,700 – well below its peak of $5,600.

This is particularly surprising given that the market environment, at first glance, would seem to support a rise in gold prices. Geopolitical tensions, rising oil prices, and an uncertain capital market environment have traditionally been favorable for gold. Yet now we are seeing the opposite. This may suggest that the underlying logic of the market has changed.

Today, gold prices are no longer driven primarily by “fear,” but by global capital flows – particularly so-called central bank flows. These movements are rooted in reserve allocation decisions by central banks and sovereign entities (between USD, gold, and other assets).

Much of the gold rally in recent years has been driven by these dynamics: de-dollarization efforts – where global central banks reduce the role of the dollar in their economies and reserves – gold purchases by emerging market central banks (such as China, Turkey, and Poland), and geopolitical diversification. The logic was straightforward: if the risk of USD-denominated assets increases, it may be worth shifting toward assets that cannot be “frozen,” such as gold.

Now, however, a reversal appears to be underway because of the Iran war: central bank flows are weakening or partially reversing. It remains uncertain whether this shift will be short- or medium-term.

The main reasons include:

- a stronger dollar and higher US yields, making USD assets more attractive again,

- increased demand for dollars due to rising oil prices and higher import financing needs,

- market stress pushing demand toward more liquid assets,

- and tactical rebalancing following previous gold accumulation, leading to normalization.

Central banks do not operate like traditional asset managers. Their decisions are governed by strict institutional frameworks that prioritize liquidity and capital preservation over return maximization. International guidelines (e.g., IMF, BIS) limit risk-taking, making allocation changes gradual and incremental.

Reserve portfolios are typically divided into two parts: a liquidity tranche, consisting of highly liquid assets for short-term needs, and an investment tranche with a longer horizon, where diversification (including gold) plays a role. This structure explains why liquid USD assets remain dominant—their operational role is difficult to replace. Gold is typically not used for immediate liquidity needs but serves as a strategic diversification tool.

What does this mean in practice?

Today, gold – during periods of war or heightened geopolitical tension – is not a classic safe haven, but rather a global macro asset primarily driven by factors such as dollar strength, the interest rate environment, and central bank allocations/flows.

Key takeaway

The relationship “war = rising gold” is not necessarily automatic. In the short term, a stronger USD, higher or non-declining interest rates, and weakening central bank flows are putting pressure on gold. At the same time, over the longer term, de-dollarization trends and the inflationary environment may continue to support the investment case for gold.

One of the key messages of the 2020s: there is no single “perfect” safe-haven asset. Central banks do not shift abruptly; instead, they adjust their portfolios gradually within existing frameworks – and this slow, structural adaptation is becoming increasingly visible in the gold market as well.

Related chart:

Turkish Central Bank’s gold reserves

Source: TCMB EVDS | Can Sezer

Jogi nyilatkozat: A blog üzemeltetője a VIG Befektetési Alapkezelő Magyarország Zrt., a szerzői az Alapkezelő munkavállalói. A weboldal kereskedelmi kommunikációt tartalmaz. A blogon megjelenő cikkek magánszemélyek szubjektív véleményét tükrözik, tájékoztatási céllal készülnek és nem minősülnek befektetési elemzésnek vagy befektetési tanácsadásnak és nem tartalmaznak befektetési ajánlást. A blog szerzői saját nevükben kereskedhetnek olyan pénzügyi és pénzeszközzel vagy más termékkel, amelyről az általuk készített cikk közöl tájékoztatást vagy véleményt. Bár a szerzők tőzsdei vagy tőzsdén kívüli kereskedés során szerzett tapasztalata a jelen blogon szereplő írásaikban is megjelenhet, de érdekeltség nem befolyásolhatja az általuk közölt tájékoztatást. A blogon megjelenő cikkekben, hírekben és tájékoztatásokban megjelenhetnek olyan társaságok, amelyek üzleti kapcsolatot tartanak fenn a VIG Befektetési Alapkezelő Magyarország Zrt.-vel vagy a blog szerzőivel akár közvetlenül, akár a VIG Group cégcsoportba tartozó más vállalkozáson keresztül. Jelen blogon megjelent cikkek nem tartalmaznak teljes körű tájékoztatást, és nem helyettesítik a befektetés megfelelőségének vizsgálatát, amelyet csak az adott befektető egyedi körülményeinek értékelésével lehet megállapítani. A megalapozott befektetési döntés meghozatalához kérjük, hogy részletesen és több forrásból tájékozódjon!

A VIG Befektetési Alapkezelő Magyarország Zrt., a blog szerkesztői és szerzői nem vállalnak felelősséget a blogon szereplő tartalom naprakészségéért, esetleges hiányosságaiért vagy pontatlanságaiért, valamint a blogcikkek alapján hozott befektetési döntésekért és a befektetési döntésekből származó bármilyen közvetlen vagy közvetett kárért vagy költségért.