What exchange rate should mark the end of the forint?

In their latest article published on Telex.hu, Zsófia Béri, Portfolio Manager at VIG Asset Management, and Bálint Jagadics, Analyst, highlight the importance of the conversion exchange rate linked to the introduction of the euro.

At first glance, the debate over adopting the euro may seem distant and technical: Maastricht criteria, central bank flexibility, fiscal deficits.

For most people, however, the issue appears in much simpler terms: how much their salary will be worth in euros, what will happen to their savings, whether prices will be rounded up, and whether buying a home will become easier or harder.

That is why the conversion rate is not merely a technical detail. It determines not only what number appears on the first euro-denominated bank statement, but also under what conditions Hungarian households and businesses begin life inside the eurozone.

The joy of the first day

The significance of the conversion rate is perhaps best illustrated through a simple real-life example. Imagine a young couple who have spent years saving for a home purchase and managed to accumulate 10 million forints. It makes a major difference at what exchange rate the country converts to the euro.

At an entry rate of around 360 forints per euro, their savings would be worth approximately EUR 27,800. At 390, only about EUR 25,600. At 400, just EUR 25,000.

At first glance, the choice seems obvious: a stronger forint appears more favourable for households. More euros would appear in bank accounts, down payments for homes would feel more attainable, and everything priced in euros – or influenced by import prices – from foreign holidays to cars and electronics, would seem cheaper.

But this only captures the very first moment of the transition. Adopting the euro is not a one-time currency exchange; it is entry into an entirely new economic system. The truly important question is therefore not how many euros appear in the account on day one, but how wages, jobs, housing prices, and corporate competitiveness evolve in the years that follow under a given exchange rate.

What looks like a gain at first may backfire later

If Hungary were to adopt the euro at an excessively strong exchange rate, Hungarian wages, rents, and corporate costs would suddenly appear much higher in euro terms. This might initially seem like good news for households, but it is only sustainable if the productivity of the economy can support such levels.

An exporting automotive supplier, for example, competes in euros. If Hungarian labour costs suddenly rise sharply in euro terms, the company may not immediately lay off workers, but it could become more cautious: postponing wage increases, reducing bonuses, or hiring fewer employees. A few years later, what seemed like a gain on the day of transition could return in the form of slower wage growth or weaker job prospects.

The opposite scenario is not painless either. Entering the eurozone at a weaker forint rate could help exporters in the short term, but it would also reduce the euro value of wages and savings held in forints. The real question is therefore not whether Hungary should prefer a strong or weak forint, but what exchange rate the Hungarian economy can sustainably support over the long term.

The housing market would also feel the impact

This is particularly important in a housing market that is already tight. According to the latest housing price data from the Hungarian Central Statistical Office (KSH), housing prices nationwide rose by 2.4% quarter-on-quarter in the fourth quarter of 2025, while annual growth reached 21%. In Budapest, the average price per square meter for used homes stood around HUF 1.2 million, with an average transaction price of approximately HUF 68 million.

In this environment, the euro itself would not automatically make housing more expensive, but it would make the Hungarian market more transparent for foreign buyers. The price of a Budapest apartment could be compared much more easily with properties in Bratislava, Zagreb, or Vienna, while exchange-rate risk related to the forint would disappear.

This does not mean foreign buyers would flood Budapest the day after euro adoption. Rather, over time, competition could intensify in an already supply-constrained market for well-located, easily rentable apartments.

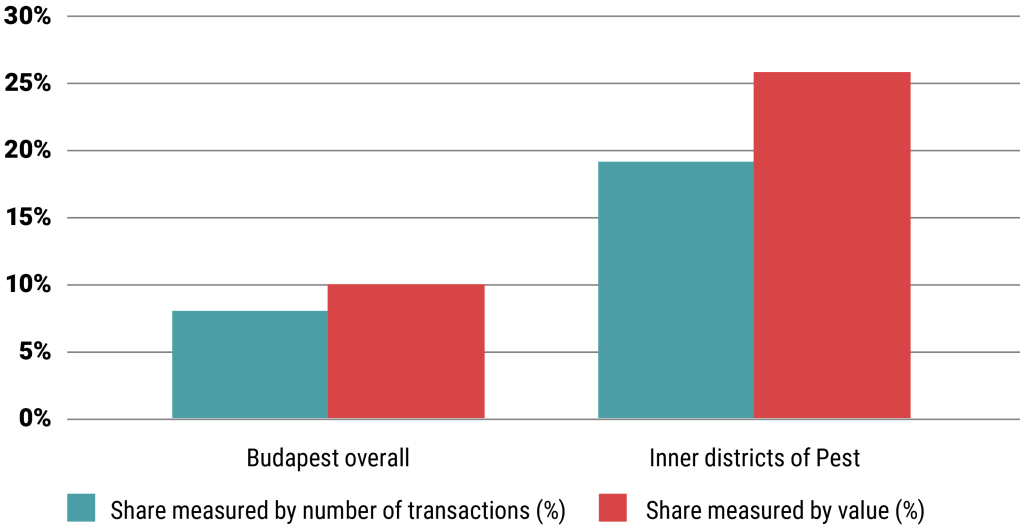

Share of Foreign Buyers in Budapest and the Inner Districts of Pest (%, 2024)

Source: KSH Housing Price Index, Q2 2025

According to KSH data on foreign buyers from 2024, foreigners accounted for 7.8% of transactions in Budapest and 10% of total market value. In the inner districts of Pest, however, their share reached 19% of transactions and 26% by value.

In other words, it is not that foreigners dominate Budapest’s housing market, but that their presence is highly concentrated – precisely in the locations where young Hungarian buyers would also prefer to purchase smaller, well-located apartments that can later be sold or rented out easily.

Trust matters for everyday prices too

For many people, however, the transition would first be felt not in the housing market, but at the grocery store.

A coffee costing 690 forints, a lunch menu for 1,990, or a haircut priced at 4,990 would all convert into awkward decimal amounts in euros. This is where the temptation to round prices emerges: instead of exact conversion, businesses may choose “cleaner” but slightly more expensive euro prices.

By itself, this would not necessarily trigger a major inflation shock. Regional experience shows that large inflationary waves are typically not caused directly by the introduction of the euro. The real issue is that people do not perceive inflation the way statistical offices measure it.

Official inflation baskets include thousands of products and services, while consumers mainly remember a handful of frequently purchased items: coffee, pastries, lunch menus, parking fees, haircuts, and small daily purchases.

If many businesses round prices upward in these everyday categories, public perceptions of inflation can deteriorate quickly, even if the overall statistical effect remains moderate. Families do not calculate how many tenths of a percentage point annual inflation increased because of the euro. What they feel is simply that “last week this coffee cost 690 forints, now it costs 2 euros.”

Even if the difference amounts to only a few hundred forints per purchase, the psychological effect can be significant because these are recurring expenses.

That is why trust matters at least as much as the exchange rate itself during euro adoption. Dual price displays, transparent conversion rules, regulatory oversight, and strong consumer protection are not mere administrative details. They help ensure that the transition is not remembered as another hidden wave of price increases.

If people see that shop prices are converted transparently, fairly, and under supervision, they are far more likely to accept the new currency.

Not a miracle cure, but a potential stabilizing force

Adopting the euro would not automatically solve Hungary’s economic problems. It would not instantly raise wages, lower housing costs, or accelerate convergence with Western Europe. But if well prepared, it could provide one important benefit: less uncertainty.

Without exchange-rate volatility, households could plan more easily over the long term. Comparing wages, prices, and savings with other European countries would become simpler. Companies would also face lower currency risk, creating a more stable environment for investment and financing.

The real question, therefore, is not whether the euro would perform miracles. It would not. The question is whether Hungary would enter the eurozone in a condition – and at an exchange rate – that the economy can sustain over the long run.

If the answer is yes, the common currency would represent not only new banknotes and new prices, but also a more predictable financial environment.

If, however, Hungary was to join too early, without proper preparation, or at an exchange rate misaligned with the economy’s real capacity, the euro would not solve the country’s existing problems. It would merely make them more visible.

Weak productivity, housing tensions, lower wage levels, or fiscal vulnerabilities would not disappear simply because calculations are made in euros instead of forints. In such a scenario, the common currency would merely reveal the same economic constraints in a different denomination.

Jogi nyilatkozat: A blog üzemeltetője a VIG Befektetési Alapkezelő Magyarország Zrt., a szerzői az Alapkezelő munkavállalói. A weboldal kereskedelmi kommunikációt tartalmaz. A blogon megjelenő cikkek magánszemélyek szubjektív véleményét tükrözik, tájékoztatási céllal készülnek és nem minősülnek befektetési elemzésnek vagy befektetési tanácsadásnak és nem tartalmaznak befektetési ajánlást. A blog szerzői saját nevükben kereskedhetnek olyan pénzügyi és pénzeszközzel vagy más termékkel, amelyről az általuk készített cikk közöl tájékoztatást vagy véleményt. Bár a szerzők tőzsdei vagy tőzsdén kívüli kereskedés során szerzett tapasztalata a jelen blogon szereplő írásaikban is megjelenhet, de érdekeltség nem befolyásolhatja az általuk közölt tájékoztatást. A blogon megjelenő cikkekben, hírekben és tájékoztatásokban megjelenhetnek olyan társaságok, amelyek üzleti kapcsolatot tartanak fenn a VIG Befektetési Alapkezelő Magyarország Zrt.-vel vagy a blog szerzőivel akár közvetlenül, akár a VIG Group cégcsoportba tartozó más vállalkozáson keresztül. Jelen blogon megjelent cikkek nem tartalmaznak teljes körű tájékoztatást, és nem helyettesítik a befektetés megfelelőségének vizsgálatát, amelyet csak az adott befektető egyedi körülményeinek értékelésével lehet megállapítani. A megalapozott befektetési döntés meghozatalához kérjük, hogy részletesen és több forrásból tájékozódjon!

A VIG Befektetési Alapkezelő Magyarország Zrt., a blog szerkesztői és szerzői nem vállalnak felelősséget a blogon szereplő tartalom naprakészségéért, esetleges hiányosságaiért vagy pontatlanságaiért, valamint a blogcikkek alapján hozott befektetési döntésekért és a befektetési döntésekből származó bármilyen közvetlen vagy közvetett kárért vagy költségért.