The Twilight of the Petrodollar and Gold’s Volatility

Global financial stability was built for decades on the 1974 Kissinger agreement. Following the 1973 Yom Kippur War, Kissinger personally mediated between Arab countries and Israel, laying the foundation for the region’s subsequent stability.

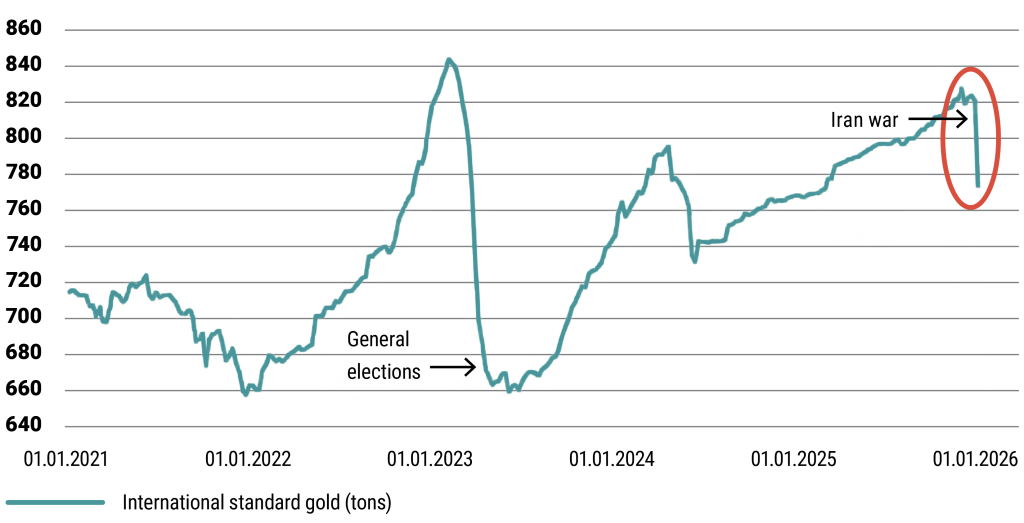

As a result, Saudi Arabia priced oil in U.S. dollars and reinvested excess profits into U.S. government securities – primarily Treasuries. Several Gulf states followed Saudi Arabia’s example, receiving in return U.S. security guarantees and a stable global order. This “virtuous cycle,” however, has been shattered by the Iranian conflict.

In recent weeks, this cycle has broken down: both export activity and reinvestment flows have come to a halt. The crisis began on the export side: due to the closure of the Strait of Hormuz, Gulf states have been barely able – or entirely unable – to ship oil. As a result, approximately 10 million barrels per day of production have been lost, eliminating oil revenues that would otherwise be recycled into U.S. debt.

The numbers tell the story: in January, these countries still held around $300 billion in U.S. Treasuries, but today they are already discussing a reassessment of their investment commitments to Washington.

Forced Sellers: From Treasuries to Gold

Importers (Turkey, India, Thailand) have found themselves in a double squeeze: oil prices above $100 and weakening currencies have significantly increased their demand for dollars.

- Bond sell-offs: Foreign central bank holdings at the Fed have declined by $82 billion, reaching their lowest level since 2012.

- Yield spike: The 10-year Treasury yield has risen from 3.9% to above 4.4%, signaling that the U.S. is no longer perceived as the ultimate “safe haven.”

Turkey and the Liquidation of Gold

Market data suggests that Turkey took drastic measures to stabilize the lira:

- Between February and the end of March, Ankara sold 52 tonnes of gold and entered into 79 tonnes worth of gold swap transactions.

- This amounts to nearly $20 billion in liquidity, contributing to gold’s 11.5% monthly decline – the worst month since 2008.

Turkish Central Bank’s gold reserves

Source: TCMB EVDS | Can Sezer

Turning Point

Since early 2025, central banks collectively have held more gold than U.S. Treasuries for the first time since 1996. While Turkey and Russia were forced sellers, flow data and Bloomberg reports indicate that China purchased a record 160,000 ounces of gold in March.

The petrodollar system was built on a political promise: the United States as a global stabilizer. By becoming a direct participant in conflict, the U.S. has undermined this foundation – at least in the short term. The share of U.S. public debt held by foreign investors has fallen to 32% from a previous 50%, suggesting that the era of unconditional trust may be coming to an end.

Henry Kissinger’s life and the legacy of realpolitik highlight that history is often shaped by a series of unintended consequences, where even the most precise strategic planning can be overridden by what Donald Rumsfeld termed “unknown unknowns.” The same applies to investing.

For investors, the lesson is clear: wisdom lies in rational optimism – accepting the role of randomness without succumbing to dogmatism. Since markets are not deterministic but probabilistic, even the most robust analysis can produce weak short-term outcomes when randomness turns against us.

This realization calls for a fundamental shift in capital market thinking:

- Think in probabilities: Instead of precise forecasts, assess the future in ranges and confidence intervals.

- Diversify relentlessly: As luck affects individual positions unpredictably.

- Avoid overconfidence: Recognize the limits of foresight.

While we cannot control luck, disciplined and structured thinking can limit losses and improve long-term outcomes. The shared lesson of history and financial markets is both a warning and a guide: you cannot control outcomes, but you can control how you make decisions – and in the long run, that is what makes the greatest difference. At VIG Asset Management, this is precisely what we strive for.

Jogi nyilatkozat: A blog üzemeltetője a VIG Befektetési Alapkezelő Magyarország Zrt., a szerzői az Alapkezelő munkavállalói. A weboldal kereskedelmi kommunikációt tartalmaz. A blogon megjelenő cikkek magánszemélyek szubjektív véleményét tükrözik, tájékoztatási céllal készülnek és nem minősülnek befektetési elemzésnek vagy befektetési tanácsadásnak és nem tartalmaznak befektetési ajánlást. A blog szerzői saját nevükben kereskedhetnek olyan pénzügyi és pénzeszközzel vagy más termékkel, amelyről az általuk készített cikk közöl tájékoztatást vagy véleményt. Bár a szerzők tőzsdei vagy tőzsdén kívüli kereskedés során szerzett tapasztalata a jelen blogon szereplő írásaikban is megjelenhet, de érdekeltség nem befolyásolhatja az általuk közölt tájékoztatást. A blogon megjelenő cikkekben, hírekben és tájékoztatásokban megjelenhetnek olyan társaságok, amelyek üzleti kapcsolatot tartanak fenn a VIG Befektetési Alapkezelő Magyarország Zrt.-vel vagy a blog szerzőivel akár közvetlenül, akár a VIG Group cégcsoportba tartozó más vállalkozáson keresztül. Jelen blogon megjelent cikkek nem tartalmaznak teljes körű tájékoztatást, és nem helyettesítik a befektetés megfelelőségének vizsgálatát, amelyet csak az adott befektető egyedi körülményeinek értékelésével lehet megállapítani. A megalapozott befektetési döntés meghozatalához kérjük, hogy részletesen és több forrásból tájékozódjon!

A VIG Befektetési Alapkezelő Magyarország Zrt., a blog szerkesztői és szerzői nem vállalnak felelősséget a blogon szereplő tartalom naprakészségéért, esetleges hiányosságaiért vagy pontatlanságaiért, valamint a blogcikkek alapján hozott befektetési döntésekért és a befektetési döntésekből származó bármilyen közvetlen vagy közvetett kárért vagy költségért.