The model portfolios have been constructed based on the VIG Investment Clock and our tactical asset allocation strategy, using following principles: we have selected 4-5 investment funds from our own range.

In all three currencies, the Conservative Portfolio targets a composition of 40% equities and 60% bonds, while the Dynamic Portfolio focuses on 60% equities and 40% bonds. The key economic factors behind these allocations include global and regional economic trends, expectations of central bank interest rate cuts, and investor sentiment.

Conservative portfolio focuses more on stability and fixed income assets (bonds), whereas dynamic portfolios aim for higher-yield outlook, using the volatility of equities. ESG considerations remain important, particularly in emerging markets and mixed-asset funds.

Investment Approach

According to our proprietary economic cycle indicator, the VIG Investment Clock, global growth prospects remain favourable. The current upswing phase of the economic cycle continues to support equity markets and commodity investments. While it is true that the U.S. – Iran conflict that erupted in late February has has caused significant turbulence, but it has not yet substantially affected longer-term economic and capital market trends.

Among stock markets, U.S. equity markets may continue to underperform relative to recent years. Further price increases in technology companies – especially those linked to artificial intelligence (AI) – appear increasingly uncertain. The return on their massive investments is being questioned by a growing number of investors, prompting a gradual shift of capital toward more traditional industries and smaller-capitalisation companies.

The energy and commodities sectors are also beneficiaries of this rotation. Companies operating in these industries – and their share prices – may gain further momentum in light of the military operations currently taking place in the Middle East.

The global oil price has risen to around USD 100 per barrel (159 litres) amid growing expectations of an escalation of the conflict, representing roughly a 50% increase during the first two weeks of March. Iran has effectively closed the Strait of Hormuz, the primary export route for oil from Saudi Arabia, Iraq, Iran, Kuwait and the United Arab Emirates, as well as for liquefied natural gas (LNG) exports from Qatar.

When oil prices rise, the effect feeds through into the prices of virtually all goods and services. It is therefore not surprising that inflation expectations have increased worldwide, which in turn supports the outlook for commodity markets.

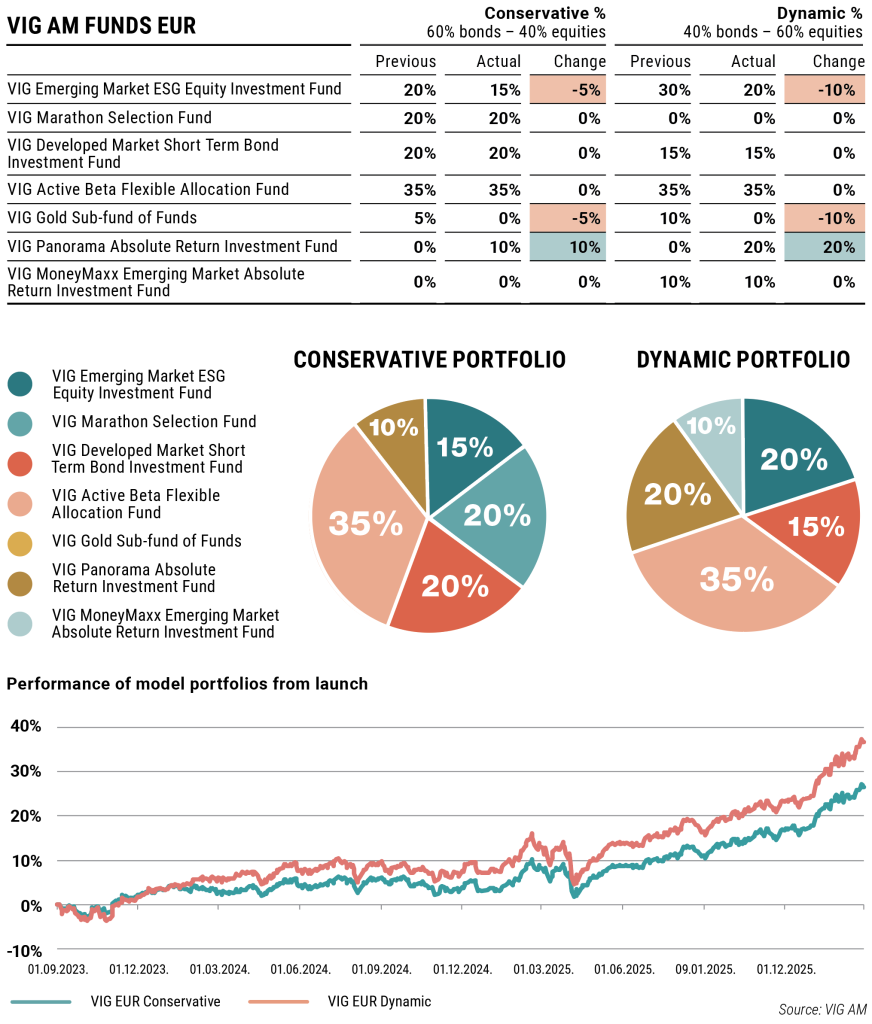

VIG EUR Portfolios

In response to market trends, we have adjusted the composition of our EUR-denominated portfolios. We have slightly reduced the weighting of the VIG Emerging Markets ESG Equity Investment Fund: due to the US-Iran conflict, investors’ risk appetite has declined, and emerging market equities are now less popular due to heightened caution.

However, due to rising expectations of „war inflation”, we have added the VIG Panorama Absolute Return Investment Fund – which has significant exposure to commodities and delivers truly outstanding performance during periods of inflation – to the portfolio.

The largest weighting (35%-35%) is still held by the VIG Active Beta Flexible Allocation Investment Fund, which invests in some of the most widely traded U.S. and European stocks: the Fund employs a selective investment strategy, which allows it, to capitalize on the ongoing rotation among equity sectors.

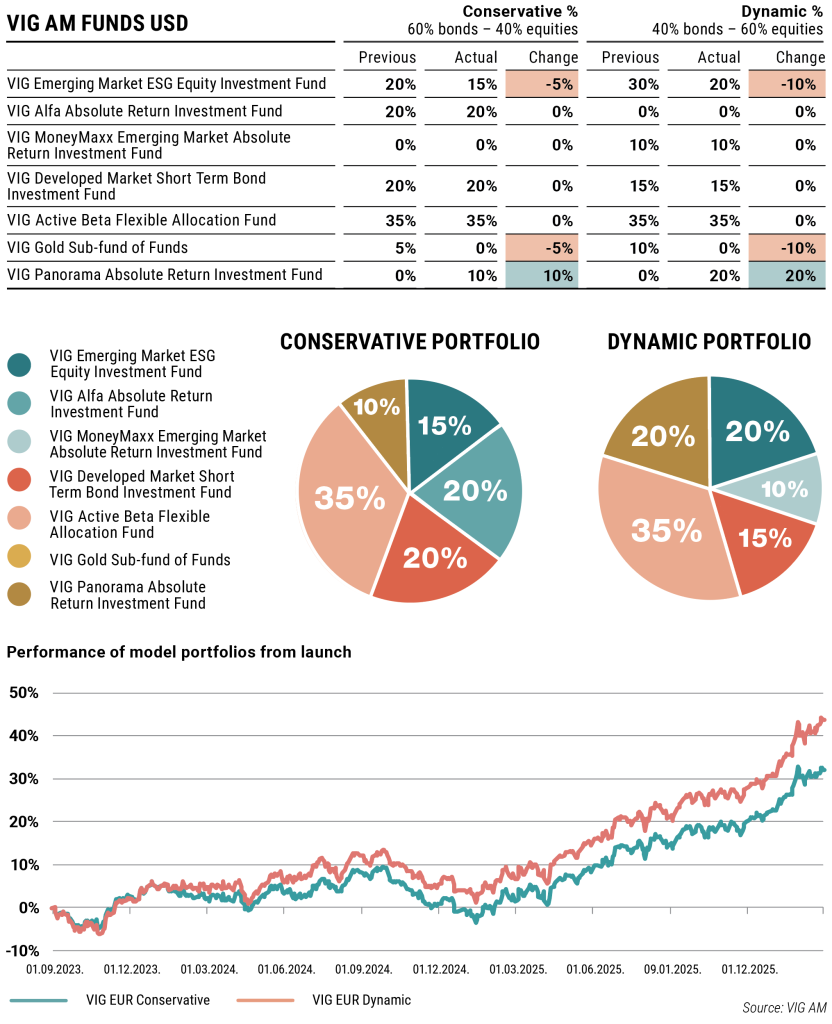

VIG USD Portfolios

We have also made changes to the tactical allocation of the dollar-based model portfolio. The largest holding remains the VIG Active Beta Flexible Allocation Fund, which holds a significant proportion of the most widely traded European stocks while implementing robust risk management.

Rising inflation expectations are again addressed through the VIG Panoráma Absolute Return Investment Fund, which has substantial exposure to commodity markets. At the same time, we have reduced our exposure to emerging market equities, which have recently become less attractive, as well as to gold investments, which now appear somewhat overvalued.

Disclaimer

This is a distribution announcement. Detailed information is needed to make a well-founded investment decision. Please inform yourself thoroughly regarding the Fund’s investment policy, potential investment risks and distribution in the Fund’s key investment information, official prospectus and management regulations available at the Fund’s distribution outlets and on the Asset Management’s website (www.vigam.hu). The costs related to the distribution of the fund (buying, holding, selling) can be found in the fund’s management regulations and at the distribution outlets. Past returns do not predict future performance. Please note that in comparison with other investment funds, the return achieved may be affected by differences in the reference index and therefore the investment policy.

The future performance that can be achieved by investing may be subject to tax, and the tax and duty information relating to specific financial instruments and transactions can only be accurately assessed on the basis of the individual circumstances of each investor and may change in the future. It is the responsibility of the investor to inform himself about the tax liability and to make the decision within the limits of the law.

The information contained in this leaflet is for informational purposes only and does not constitute an investment recommendation, an offer or investment advice. VIG Asset Management Hungary Closed Company Limited by Shares accepts no liability for any investment decision made on the basis of this information and its consequences.

The Asset Management’s license number for managing alternative investment funds (AIFM) is: H-EN-III-6/2015. The Fund Manager’s license number for UCITS fund management (collective portfolio management) is: H-EN-III-101/2016.