CEE inflation outlook

Progress Made, Challenges Ahead

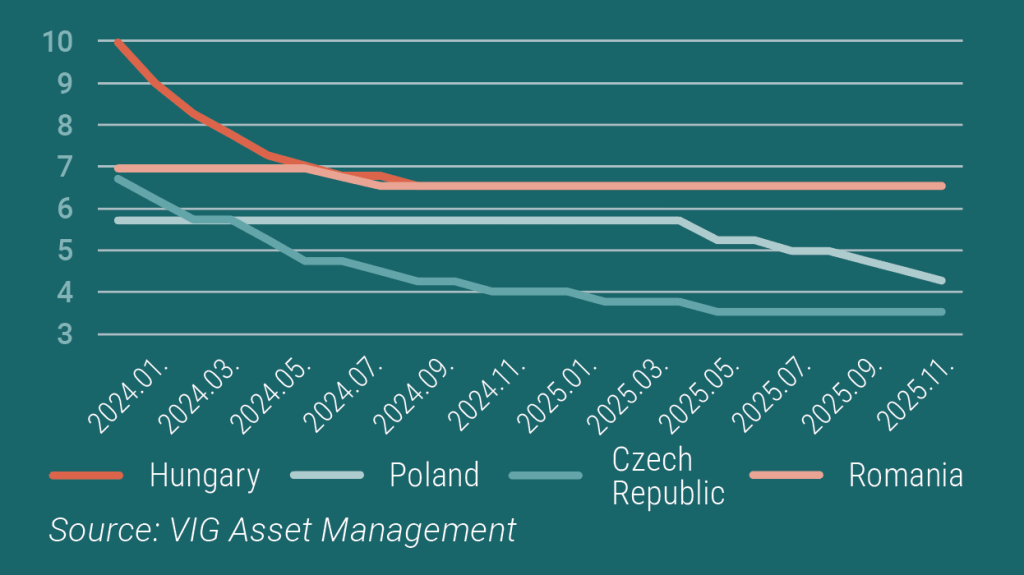

Disinflation remained the dominant theme across Hungary, Czech Republic and Poland throughout 2025. As winter set in, price pressures moderated further, and December inflation is expected to fall comfortably within central bank tolerance ranges. With this, regional easing cycles are nearing completion, while both the Czech and Hungarian central banks have already maintained a steady policy stance for some time. Although inflation targets are now within sight, 2026 is unlikely to mark full convergence for much of the region.

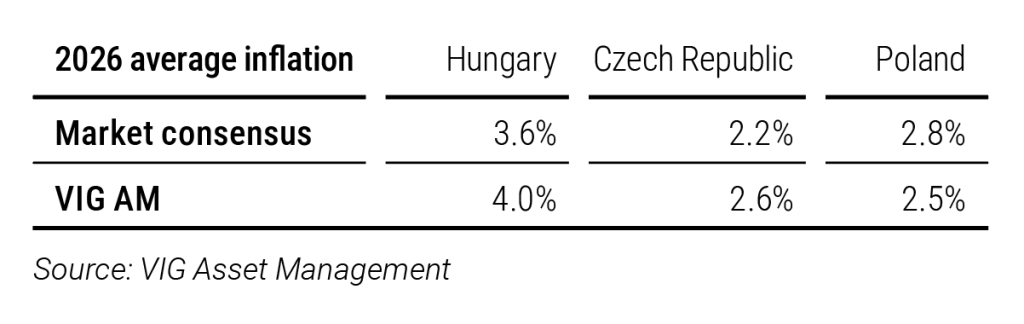

In the Czech Republic, the 2026 inflation outlook will be shaped primarily by the development of household energy costs, as the risks surrounding the 2025 parliamentary elections will already be behind us. Czech households face some of the highest energy costs in the EU, making cost reduction a central topic in the October election campaign. Both the government and major energy suppliers have been exploring measures to mitigate rising costs, several of which could positively influence the 2026 inflation trajectory. The central bank’s rate-cutting cycle has ended, and future moves will likely hinge on how energy costs evolve.

In Hungary, next year’s inflation dynamics will be determined primarily by the April elections and the potential extension of related government measures. Many of the policies designed to temporarily suppress inflation are scheduled to expire in 2026, meaning that the lower inflation seen in the run-up to the election will likely give way to a trend-like acceleration in the second half of the year. The magnitude of the rebound is uncertain, but artificially depressed inflation in the first half will almost certainly result in lower average inflation in 2026 than in 2025. Consequently, a renewed round of rate cuts is unlikely in the first half of the year. Service inflation is expected to remain sticky in 2026, leaving our forecast above market consensus. A stable political environment and a sustained decline in household inflation expectations will be essential prerequisites for restarting monetary easing.

In Poland, the successes achieved this year have played a major role in positioning the Polish central bank to be the first in the region to reach its inflation target in 2026. However, several risks threaten next year’s inflation path. Fiscal easing and strong domestic consumption may constrain the fight against inflation. Reducing household energy costs remains a priority in Poland as well, especially since the energy price freeze expires at the end of this year. The President nonetheless aims to reduce energy costs for both households and businesses through new decrees thereafter. Having curbed inflation more effectively than its regional peers, the Polish central bank may be approaching the end of its easing cycle.

Romania is the outlier in the region, as its inflation trajectory has diverged sharply due to government measures implemented in 2025. In summer 2025, the Romanian government introduced significant tax increases to restore fiscal balance. VAT was raised from 19% to 21%, the energy price cap was removed, and excise taxes were increased as well. As a result, Romania’s fight against inflation will lag regional peers by around one year: the high-inflation period that began in July 2025 will only end in summer 2026, after which the continuation of the rate-cutting cycle may once again become feasible.

Central bank base rates (%)

További cikkekBefektetési Kilátások 2026 Dokumentum megtekintéseLetöltés

Ez egy forgalmazási közlemény. A megalapozott befektetési döntés meghozatalához részletes tájékozódásra van szükség. Az Alap befektetési politikájáról, forgalmazási költségeiről és a befektetés lehetséges kockázatairól részletesen tájékozódjon az Alap forgalmazási helyein és az Alapkezelő weboldalán (www.vigam.hu) található Kiemelt Információkból, hivatalos tájékoztatóból és kezelési szabályzatból. A befektetési alap forgalmazásával (vétel, tartás, eladás) kapcsolatos költségek az alap kezelési szabályzatában és a forgalmazási helyeken megismerhetők. A múltbeli teljesítmény alapján nem jelezhetőek előre a jövőbeli hozamok. A befektetéssel elérhető jövőbeni hozam adóköteles lehet, az egyes pénzügyi eszközökre, ügyletekre vonatkozó adó- és illeték információkat pedig csak az egyes befektetők egyedi körülményei alapján lehet pontosan megítélni, ami a jövőben változhat. A befektető feladata, hogy tájékozódjon az adókötelezettségről. Jelen tájékoztatóban szereplő adatok kizárólag információs célokat szolgálnak és nem minősülnek befektetési ajánlásnak, ajánlattételnek vagy befektetési tanácsadásnak. A VIG Befektetési Alapkezelő Magyarország Zrt. nem vállal felelősséget a jelen tájékoztatás alapján hozott befektetési döntésért és annak következményeiért.

Az Alapkezelő alternatív befektetési alap kezelésére (ABAK) vonatkozó engedélyének száma: H-EN- III-6/2015. Az Alapkezelő ÁÉKBV-alapkezelési (kollektív portfóliókezelési) engedélyének száma: H- EN-III-101/2016.