Successful monthly tactical asset allocation in 2025

Global markets in 2025 were shaped by investor expectations surrounding the inauguration of the new U.S. president, the uncertainty triggered by an emerging trade war, and the subsequent wave of optimism that drove equities to new record highs.

The gradual weakening of the U.S. dollar and a strong rally in gold further supported market sentiment. AI-driven innovation once again propelled the U.S. technology sector to the forefront, with the “Magnificent 7” companies—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla—delivering particularly strong performance. Although the announcement of new US tarrifs in April caused a brief but sharp correction, markets stabilised quickly and risk appetite strengthened again in the second half of the year. Emerging markets—led by the CEE region—outperformed, supported by attractive valuations, improving earnings expectations and a more stable macroeconomic backdrop.

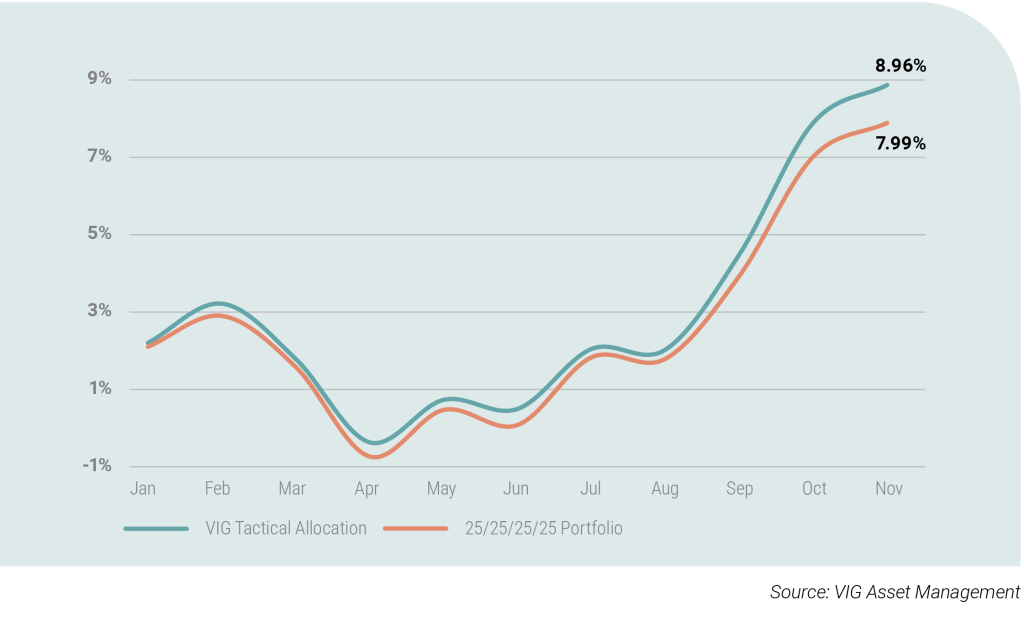

Following strong results in 2023 and 2024, VIG AM’s monthly tactical asset allocation continued to adapt effectively to rapidly changing market conditions in 2025. Supported by our Investment Clock framework and the asset-class-specific Quadrant analysis, our monthly investment process resulted in a model portfolio that outperformed its benchmark by 87 basis points in EUR terms by the end of November 2025 (benchmark allocation: 25% money market, 25% bonds, 25% commodities, 25% equities), clearly reflecting the success of our monthly tactical decisions.

The 8.96% nominal EUR return and the strong relative performance were driven primarily by commodity and equity allocation decisions. The underweight in commodities, combined with the timely downgrade and subsequent upgrade of gold—particularly during the autumn price rally—provided a meaningful contribution to returns. Within equities, the overweight in CEE markets—2025’s best-performing equity region—and the underweight in European equities, which performed well early in the year, but lagged thereafter, were key performance drivers. The persistent strength of U.S. equities and our summer underweight position had only a limited negative impact on overall returns, as the weaker dollar helped cushion the effect.

További cikkekBefektetési Kilátások 2026 Dokumentum megtekintéseLetöltés

Ez egy forgalmazási közlemény. A megalapozott befektetési döntés meghozatalához részletes tájékozódásra van szükség. Az Alap befektetési politikájáról, forgalmazási költségeiről és a befektetés lehetséges kockázatairól részletesen tájékozódjon az Alap forgalmazási helyein és az Alapkezelő weboldalán (www.vigam.hu) található Kiemelt Információkból, hivatalos tájékoztatóból és kezelési szabályzatból. A befektetési alap forgalmazásával (vétel, tartás, eladás) kapcsolatos költségek az alap kezelési szabályzatában és a forgalmazási helyeken megismerhetők. A múltbeli teljesítmény alapján nem jelezhetőek előre a jövőbeli hozamok. A befektetéssel elérhető jövőbeni hozam adóköteles lehet, az egyes pénzügyi eszközökre, ügyletekre vonatkozó adó- és illeték információkat pedig csak az egyes befektetők egyedi körülményei alapján lehet pontosan megítélni, ami a jövőben változhat. A befektető feladata, hogy tájékozódjon az adókötelezettségről. Jelen tájékoztatóban szereplő adatok kizárólag információs célokat szolgálnak és nem minősülnek befektetési ajánlásnak, ajánlattételnek vagy befektetési tanácsadásnak. A VIG Befektetési Alapkezelő Magyarország Zrt. nem vállal felelősséget a jelen tájékoztatás alapján hozott befektetési döntésért és annak következményeiért.

Az Alapkezelő alternatív befektetési alap kezelésére (ABAK) vonatkozó engedélyének száma: H-EN- III-6/2015. Az Alapkezelő ÁÉKBV-alapkezelési (kollektív portfóliókezelési) engedélyének száma: H- EN-III-101/2016.